Investment savings book: set up, inheritance and interest

Savings book – The savings book, almost every second German owns a savings book, currently there are almost 223 billion euros that are stored in Germany on savings books. The savings book offers, especially for young people a good start by the mental obligation to put money back regularly. The big disadvantage is that interest rates are currently low, even close to zero.

Back to the Capital Investment editorial.

Savings book: risk and return

Anyone setting up their first savings account will have many questions at first:

- Is a savings account at the savings bank free of charge?

- Which bank gives the most interest on savings accounts?

- What is the passbook?

- Can I transfer money to a savings account online?

The classic savings book is suitable for the steady accumulation of assets. You regularly pay in your monthly savings contribution, for example through your salary. Often, account management is free and every euro you deposit earns interest, albeit small.

A savings account is easy to set up for pretty much anyone. With the way to the bank or the online setup via a direct bank, possible for every saver. The flexible availability of the capital gives the small saver security. Due to the interest rates, however, the investment income is very low, there are almost no profits. The yield of savings accounts is very low and therefore there is almost no risk (also due to the usual bank protection by the government). As said, there is still the big disadvantage, the very low investment returns.

Savings book facts

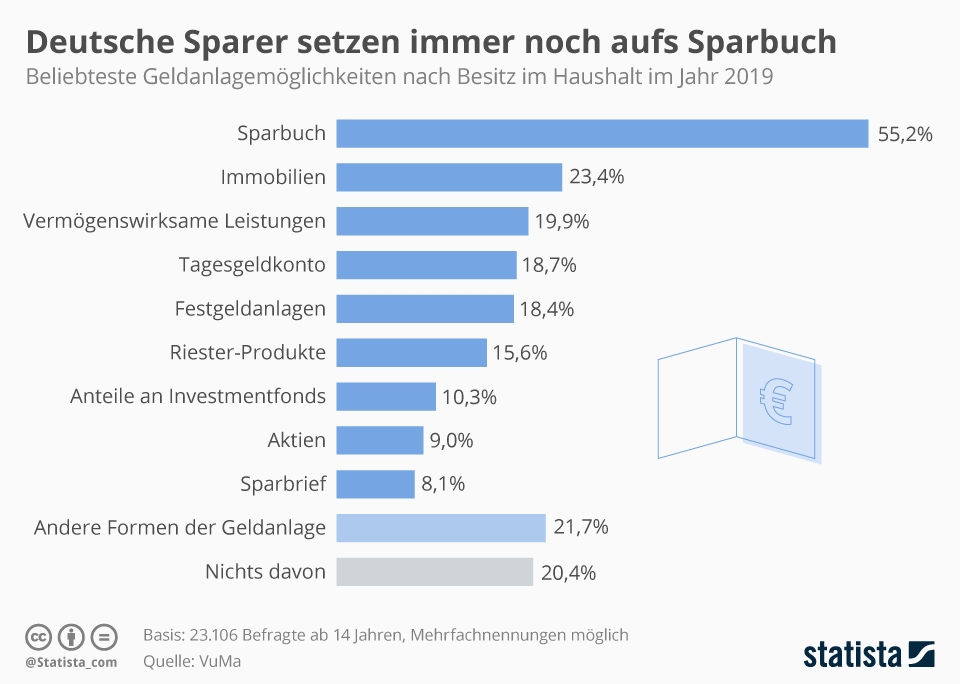

Did you already know? The savings book is the most popular investment for Germans.

Source: Statista

The most important 3 facts about the savings book:

- Possibility to invest first capital stock

- No (extremely low) risk of default

- Available for everyone

The savings book offers a safe investment and is a good option, without risk, especially for people who want to build up their first, small capital stock.

Advantages

- Anyone can set up a savings book

- Direct banks or on-site in the district

- Safe investment with minimal risk

- Flexible deposits possible at any time

- No predefined term with most providers

Disadvantages

- Low interest rates on savings books, therefore almost no investment income and yields

- Little flexibility (outside availability)

Many young people no longer have their own savings book. But what happens when you inherit a savings book?

Inherited savings book, what to do?

Savings accounts are falling over, as previously mentioned, 223 billion euros are currently still on the books. One of the reasons is, for example, the fear of price losses, for example, on the stock market when trading shares, many investors want security above all. That is why many books are inherited.

To close a savings account at your local bank, you must present the following documents to the local advisor:

- Passbook

- Identity card

- Death certificate of the deceased

- Will with opening record(certificate of inheritance if there is no will)

Read more tips on inheritance & legacy here.

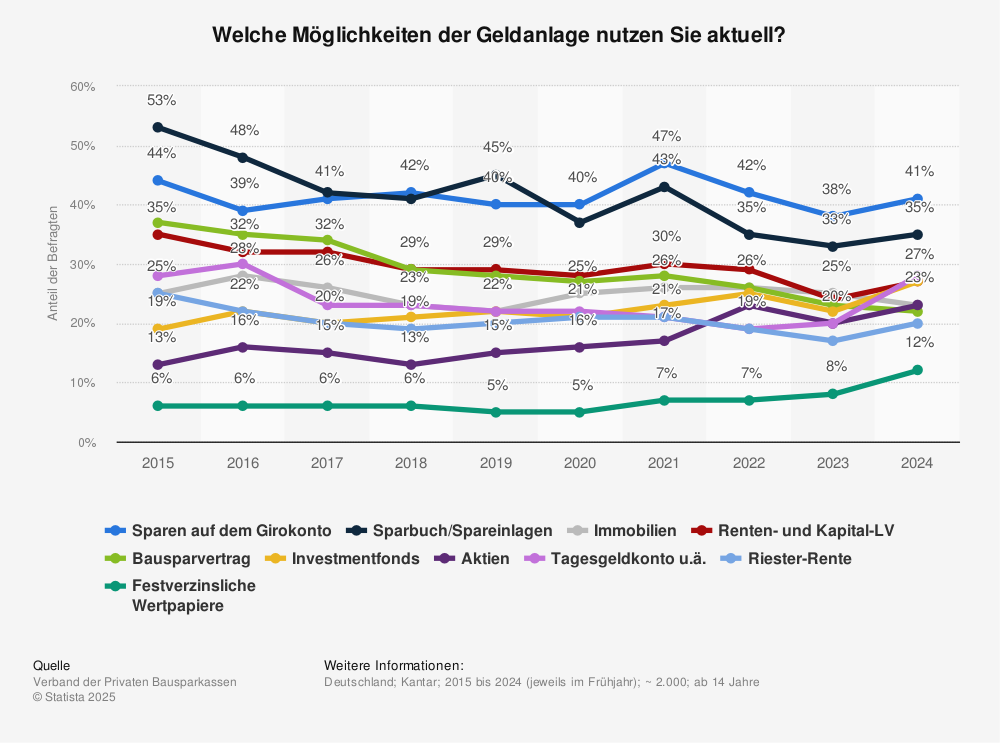

Statistics: Saving in Germany

The chart shows the proportions of households that invested in the following types of investments in 2019.

Student apartment as a capital investment: investing, renting & managing - investing with just 5,000 euros

Family Foundation for Real Estate: Interview with Stephan Czaja on the new "One" project

Real Estate Podcast: The 9 best podcasts on Apple, Spotify & Co. - prices, management, investment

Becoming a self-employed designer in the high fashion sector

Perfume online store: Fragrances for him, her & you! Top brands & rating - by FIV

Perfume subscription in the store: subscribe to your favorite fragrance and save 5% - Tip

Redman: Hip hop legend back on tour + Living modestly despite millions + Legendary MTV Cribs

Kids learn real estate: Book tip! Timmy's Adventures (in German)

10 cheap perfumes: recommendation from the fragrance expert: Versace, Jnon Montblanc & Co.

Roof tent comparison: top roof tent manufacturers for campers