Deposits rising as interest rates fall? Overnight money is more popular than ever, as we will see in later infographics and comparisons. Overnight money has the unbeatable advantage of being extremely safe due to bank deposit insurance and government bailouts, and flexible availability, unlike investing in a fixed deposit account with a binding term. But what is call money? What is a call money account? Where is the best overnight money for investors? Who has the best interest rates for overnight money? Is a call money account free? What exactly is a call money account? What’s the difference between a current account and a call money account? Together, we take a look at the advantages and disadvantages of overnight deposit accounts.

Call money is absolutely easy to set up, often the offer is already included in the account opening. Your deposited capital is available at any time and for the start with call money you need only low investment income or income.

Due to the current interest rate development, as can be seen later in the statistics, the capital increase via the overnight money is only worthwhile from very high amounts of money. For this you have a very low, almost no risk in your investment. The current yield of call money is as described very low, which is little to no risk, but you will hardly make any profit. Overnight money is like time deposits and savings accounts easy to set up in many bank branches and of course online. Your capital is available at any time.

Facts about call money

The most important 3 facts about call money:

Available for everyone

Constant availability of your money

Low return

Call money is a flexible savings option for small savers. You can access your money at any time, but the returns are more moderate than with fixed-term deposits.

Capital can be called up and is available at any time

No large equity capital required for the start

Low risk

Disadvantage of the call money account

Yield only with large sums of money

Only one disadvantage, but it is precisely the return that is the focus of investment. If you want to play it safe, overnight money is a good, safe and flexible investment. Those aiming for greater profits should also look at alternatives to overnight money.

Statistics and infographics

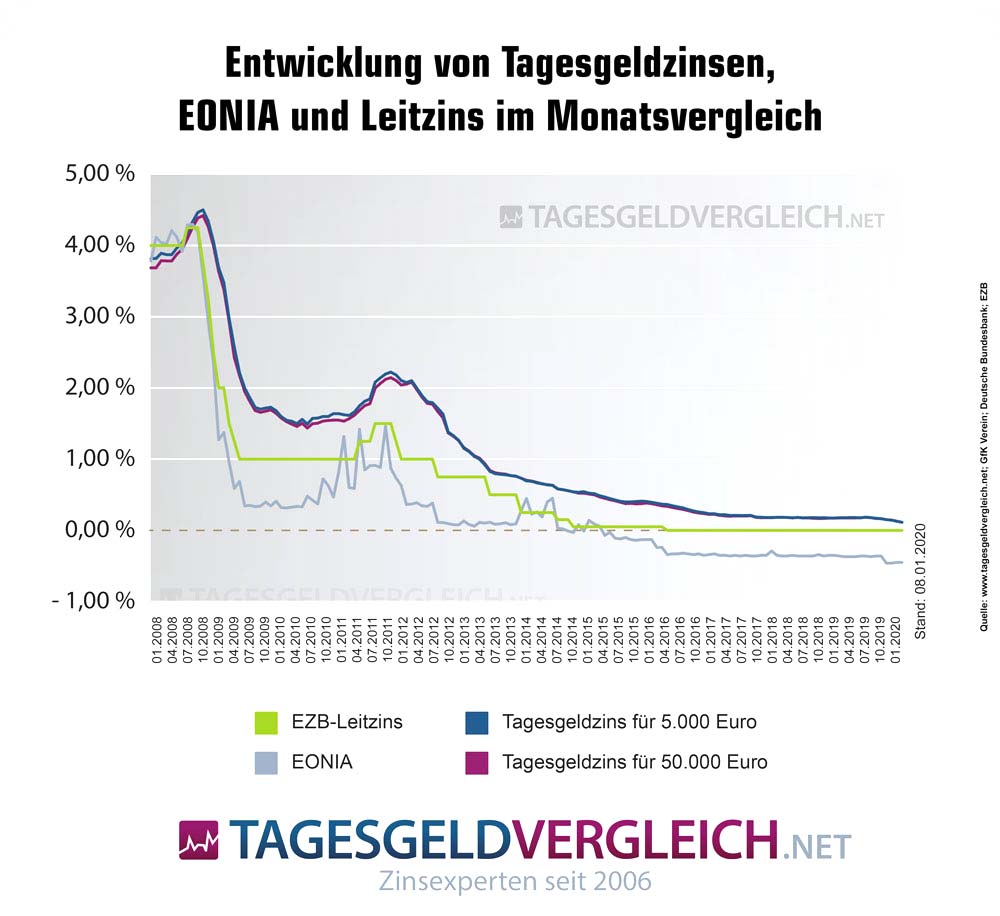

Call money comparison: Interest rate development from 120+ banks

The basis of the interest rate statistics are currently 12 tested call money accounts, which you can also find in all call money comparisons.

2008 by 4.15%

2010 by 1.12%

2012 by 1.22%

2014 by 0.39

2016 by 0.12%

2018 by -0.03%

2020 by -0.08%

Source: Tagesgeldvergleich.net

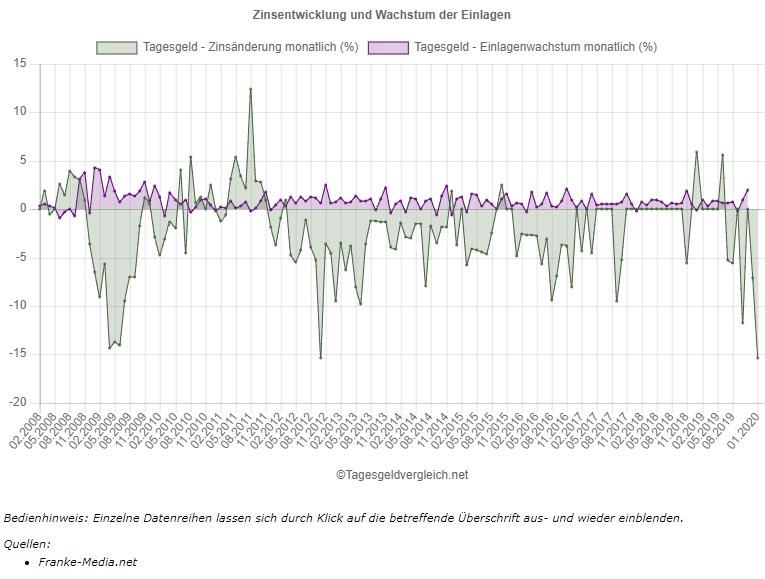

Comparison of interest rate development and amount of savings deposits

How do interest rate trends compare with the level of deposits? Normally, one should generally be able to assume that the falling interest rates, which are currently dependent on the interest rate situation, will result in a corresponding decline in the interest of savers.

However, as you can see from the chart, this is not necessarily the case, as a look at the infographic below shows. In the chart you can see how the interest rates on call money accounts have been falling steadily since the beginning of 2012, but the amount of deposits of private households with daily maturity almost always rises. As we have already noted on the subject of savings accounts, this is mainly due to the scepticism of savers towards the stock market and the economy.

Source: Tagesgeldvergleich.net

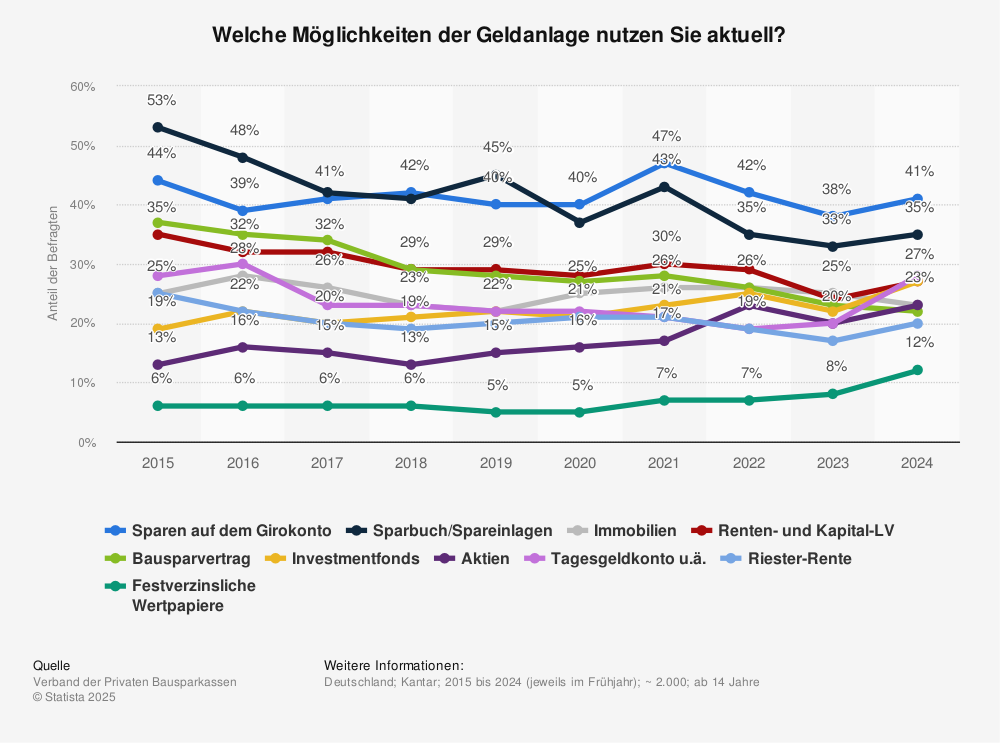

Call money in the top 3 investments

What investment options do Germans currently use? Call money is one of the top 3 forms of investment in this country.

We may request cookies to be set on your device. We use cookies to let us know when you visit our websites, how you interact with us, to enrich your user experience, and to customize your relationship with our website.

Click on the different category headings to find out more. You can also change some of your preferences. Note that blocking some types of cookies may impact your experience on our websites and the services we are able to offer.

Essential Website Cookies

These cookies are strictly necessary to provide you with services available through our website and to use some of its features.

Because these cookies are strictly necessary to deliver the website, refusing them will have impact how our site functions. You always can block or delete cookies by changing your browser settings and force blocking all cookies on this website. But this will always prompt you to accept/refuse cookies when revisiting our site.

We fully respect if you want to refuse cookies but to avoid asking you again and again kindly allow us to store a cookie for that. You are free to opt out any time or opt in for other cookies to get a better experience. If you refuse cookies we will remove all set cookies in our domain.

We provide you with a list of stored cookies on your computer in our domain so you can check what we stored. Due to security reasons we are not able to show or modify cookies from other domains. You can check these in your browser security settings.

Google Analytics Cookies

These cookies collect information that is used either in aggregate form to help us understand how our website is being used or how effective our marketing campaigns are, or to help us customize our website and application for you in order to enhance your experience.

If you do not want that we track your visit to our site you can disable tracking in your browser here:

Other external services

We also use different external services like Google Webfonts, Google Maps, and external Video providers. Since these providers may collect personal data like your IP address we allow you to block them here. Please be aware that this might heavily reduce the functionality and appearance of our site. Changes will take effect once you reload the page.

Google Webfont Settings:

Google Map Settings:

Google reCaptcha Settings:

Vimeo and Youtube video embeds:

Other cookies

The following cookies are also needed - You can choose if you want to allow them:

Privacy Policy

You can read about our cookies and privacy settings in detail on our Privacy Policy Page.